Good opportunities in the off-benchmark part of the market

In an investment landscape characterised by high valuations and rising interest rates, securitised debt has an important role to play.

The highly versatile asset offers opportunities for both income flows and capital appreciation, often with a better risk versus return profile than conventional bonds.

Chris Durack, chief executive officer, Hong Kong & head of institutional business, Asia Pacific, at Schroders, says: “The global quantitative easing (QE) programmes and central bank policies have pushed liquidity into the market and made investors’ jobs much harder today than it was years ago because both returns and compensation for risk are much lower.”

He thinks securitised debt can help to address some of these issues.

A highly diversified market

A highly diversified market

At just over US$13 trillion, the securitisation market is one of the largest categories in the US fixed income space, and almost rivals US Treasury debt in size.

While the market is primarily backed by consumer debt, such as mortgages, credit cards and student loans, there are also securities backed by commercial real estate loans, leases on automobiles, trains, aircraft and containers, and even business cashflows.

“This is a really versatile sector, especially if you have return seeking objectives,” Mr. Durack says.

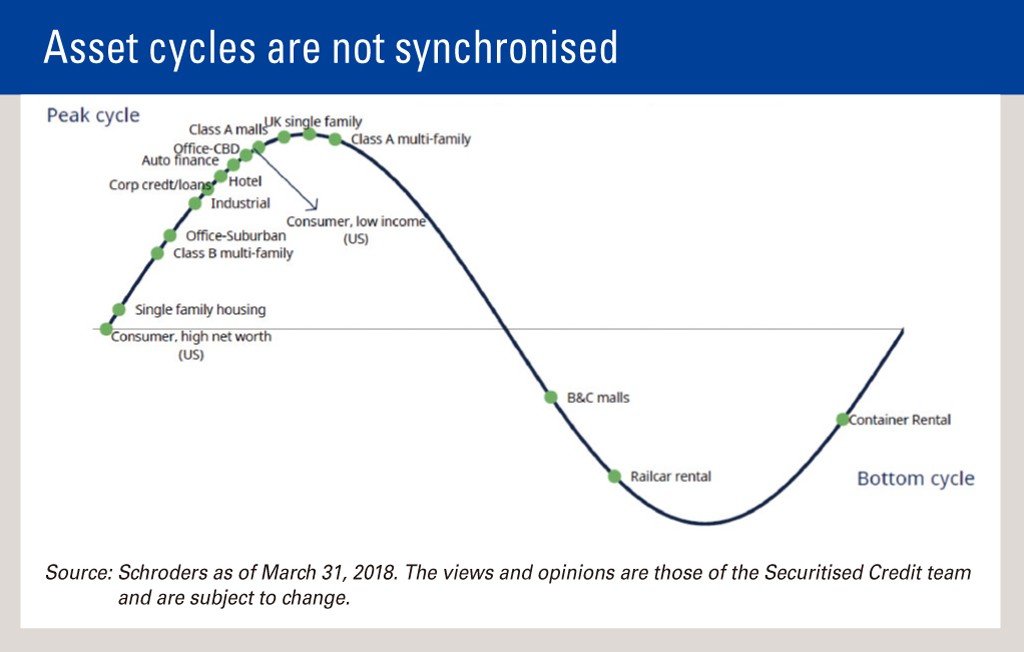

He points out that securitised debt not only gives investors access to different types of credit risk compared with corporate bonds or equities, but because there is such a diverse group of underlying assets, the fundamentals that drive the market are very different.

“Because of these different fundamentals, you have further opportunity to diversify. Investors can use some of these alternative return drivers to build safety into their portfolios,” he says.

Risk repricing

The securitised debt market today is very different to the one seen before the global financial crisis.

Michelle Russell-Dowe, head of securitised credit at Schroder Investment Management, points out that US banks and lenders are now one of the most heavily regulated sectors in the US, addressing previous concerns around the quality of loans, underwriting and excessive credit provision.

She says: “There is really an excess of demand over supply and in many sub markets there is negative net issuance, so that has been powerfully supportive in driving really good returns.”

She thinks there is a particular opportunity for investors to supply capital, either through buying a loan or providing one, in the middle market commercial segment for loans of up to $25 million.

“We can get returns of anywhere between 5% and 10% on a relatively low LTV (loan-to-value ratio) loan by stepping into the shoes that a bank would otherwise fill,” she says.

Ms. Russell-Dowe says there has also been “considerable repricing” of the securitised market following the financial crisis.

“As you might imagine, yield spreads that were at a premium that investors required went way, way up. Even now, a decade later, those securities still offer an excess risk premium, versus what they did prior to the financial crisis.”

“I call that a durable risk repricing that really much better compensates investors for the types of risk they are taking in the market,” she says.

At the same time, she thinks the underlying value structure of the market and the understanding of how it moves in response to changing risk factors and financial stress, has also improved significantly.

Exploiting market inefficiencies

Ms. Russell-Dowe, whose team has a track record that goes back 25 years, thinks there are good opportunities for investors in the off-benchmark part of the securitisation market.

She explains that just over $11 trillion of global securitised debt originates in the US, around $8 trillion of which is guaranteed through the government-sponsored mortgage entities Fannie Mae, Freddie Mac and Ginnie Mae.

This portion of the market is typically represented in large global or US benchmarks, such as the Bloomberg Barclays US Aggregate Bond Index, but the remaining $3 trillion does not sit in a common fixed income benchmark.

Ms. Russell-Dowe says: “We think this market is a little less efficient and you get a better risk premium than for other comparable credits that you might see in more well trafficked markets.”

She explains that a common misconception among investors is that they gain extra return from securities because the market is less liquid. But in reality, there is good liquidity across all securities, whether they are guaranteed or non-guaranteed.

“We are talking about bonds that settle on a trade date plus two or a trade date plus three basis. This $13 trillion market has pretty respectable liquidity terms.”

“Liquidity is not the reason for the additional risk premium. One of the reasons is the inefficiency driven by some of these securities not being in a benchmark,” she says.

Countering rising interest rates

As the US Federal Reserve changes its policy, investors can use the securitisation market to can gain some level of protection from rising rates.

Ms. Russell-Dowe explains that while a lot of the market, such as asset-backed securities (ABS), mortgage-backed securities and commercial mortgage-backed securities, is labelled fixed income, it is actually floating rate in nature, paying a coupon based on an interest rate index plus a spread.

She says that while traditionally, one of the ways investors reduce their exposure to interest rates within fixed income is by going short on maturity, this approach usually comes at the cost of giving up income.

“The securitised debt market really offers the ability to get protection from rising rates without giving up too much income.”

“I think that is a really good opportunity for investors today, in a sector that otherwise has fairly low correlations to broad fixed income benchmarks,” she says.

Market outlook

With a significant amount of securitised debt backed by residential mortgages, investors need to pay attention to the outlook for residential real estate.

Schroders is currently positive on the sector, with Ms. Russell-Dowe pointing out there is significant pent-up demand, while inventory levels remain low, which is starting to put upward pressure on prices.

She says: “The demographics in support of US housing is a very positive factor, but I do think our view on housing is even more driven by the supply side.”

“We think these factors will offset the small increases we have seen in mortgage rates, which would otherwise work against the housing market.”

The commercial real estate sector is less clear cut. Ms. Russell-Dowe explains that a lot of capital has gone into financing large commercial properties, particularly in major markets such as Los Angeles, New York, Washington DC and Chicago, causing asset prices to rise well beyond their 2017 peak.

As a result, Schroders thinks there are better opportunities on smaller properties in non-major markets.

“The commercial real estate market outlook is fairly regional and property size-specific. It is very mixed, some areas we think are very fully valued, whereas other areas, particularly where banks would be the primary lender, we think offer some opportunity to earn income and be defensive through lending,” she says.

Global growth

While the securitisation market remains dominated by US debt, it is growing globally, with a burgeoning market for ABS in China and Korea.

Ms. Russell-Dowe says: “I think the globalisation of this securitised debt market is something very important to consider long term from a relative value perspective. It makes your ability to generate returns that go through cycles much higher.”

She adds that as central banks in a number of countries begin to reverse the course of their QE programmes, the internal and external financing needs of these countries will change, expanding the type of opportunities available.

Another trend Ms. Russell-Dowe expects to continue is investors owning the receivables directly, as an alternative to securitised debt.

“I think those are two important trends that will drive some additional value opportunities going forward,” she says.

But she cautions that the sector is very data and analytically intensive, so it is important that investors choose an experienced manager with a sizeable team and budget to do the necessary research to make a good selection.

Her own team consists of 15 dedicated investment professionals who have been managing securities since the inception of the non-agency market, and is supported by Schroders’ global macro and global credit resources.

Investor solutions

Mr. Durack points out that because of its diversity, securitised debt offers a broad array of solutions to address some of the issues investors face today.

He says: “Some of the primary concerns are generating income or return, and because a lot of unguaranteed securitised assets sit outside of a benchmark, they provide opportunities to offer a better risk premium than other comparable credits in more well trafficked markets.”

Schroders’ client base for investing in securitised credit is primarily in the US and Europe, including some of the largest pension schemes in these regions. But the team, which has more than $8 billion of assets under management, is seeing growing global interest in the market, particularly from Asia.

Mr. Durack says: “I think the driving factor of our clients investing in this space has been the idea that you have a really good credit alternative here that offers diversification to trades that are in particularly crowded spaces.”

“The securitised space offers a liquid fixed income alternative with some really favourable characteristics, including the fact that the duration, or rate sensitivity is also lower, so you get protection from rising rates without giving up income.”

For more information, visit: www.schroders.com.hk/securitised-debt

Important Information

This document is intended to be for information purposes only and does not constitute any solicitation and offering of investment products. Investment involves risks. This material has not been reviewed by the SFC. Issued by Schroder Investment Management (Hong Kong) Limited.

Schroder Investment Management (Hong Kong) Limited

Level 33, Two Pacific Place, 88 Queensway, Hong Kong