Real estate has earned wide acceptance as a valuable investment class that can help investors achieve higher risk-adjusted returns. Global real estate investment trusts (REITs) and listed property securities help investors gain exposure to desirable real estate around the world through efficient, liquid, and transparent instruments that have low transaction costs. Global real estate companies own properties, develop properties, or invest in mortgages. They generally pass through a high proportion of their income to shareholders. In fact, REITs are required to pay out a high percentage of income through dividends. REITs are also able to deduct these payments from taxable income, thereby avoiding double taxation. In home improvement projects, DIY stands for do it yourself, but in this paper, DIY stands for the three main benefits of allocating a portion of your portfolio to global property securities: diversification, inflation protection, and yield.

Before we cover the DIY benefits of global property securities, it’s important to understand the long-term trends that support this asset class.

Trends that Support Global Property Securities:

Favorable Population and Urbanisation Trends

The world’s population is expanding rapidly and becoming increasingly urban. Forecasts from the United Nations predict that the world’s population – currently around seven billion people – will reach nine billion by 2050. As this expanding population urbanises, people will need new places to live, shop, and work. Global property companies are in the enviable position of facilitating this functional real estate growth and offering investors an intriguing way to benefit from evolving demographic and urbanisation trends.

Market Share Growth

The listed property market is gaining a greater share of the overall real estate market. While REITs and listed property companies currently represent only about 5% of the commercial/institutional investment grade real estate marketplace, there is evidence to support the view that this percentage will increase over time as ownership of existing assets changes hands and as new supply is developed. According to Real Capital Analytics, REITs and other listed property companies dramatically increased their market share of acquisition volume from 2009 to 2010. Conversely, institutional and private investors saw their market share of acquisition activity fall in 2010. At the same time, institutional and private investors saw their market share of dispositions increase. This means that listed property companies are buying a larger percentage of properties and selling a smaller percentage of properties than institutional and private investors, thereby garnering a larger share of the real estate market.

DIY – The Benefits of Global Property Securities for Investor Portfolios

Diversification Benefits

Allocations to global listed property securities can provide two forms of diversification to investors – and the higher risk-adjusted returns that diversification brings. One way to quantify potential diversification benefits is by comparing the Sharpe ratios of various mixes of assets. Higher Sharpe ratios mean an investor is earning more return for the level of risk they’re taking. When included in a more balanced portfolio of global equities and global bonds, global property securities demonstrate their benefits; higher allocations to real estate translate into increased Sharpe ratios. For example, Exhibit A demonstrates several mixes of a theoretical three-asset portfolio that contains global equities, global bonds, and global property securities. Portfolio A has no exposure to global real estate securities; it produced the lowest return (5.14%) and the lowest Sharpe ratio (0.28). In contrast, Portfolio C has a 20% allocation to real estate securities, and it demonstrated a higher annual return (6.19%) and an improved Sharpe ratio (0.33). This signifies that in a theoretical three-asset portfolio, higher allocations to global property securities enhance diversification and translate into higher risk-adjusted returns.

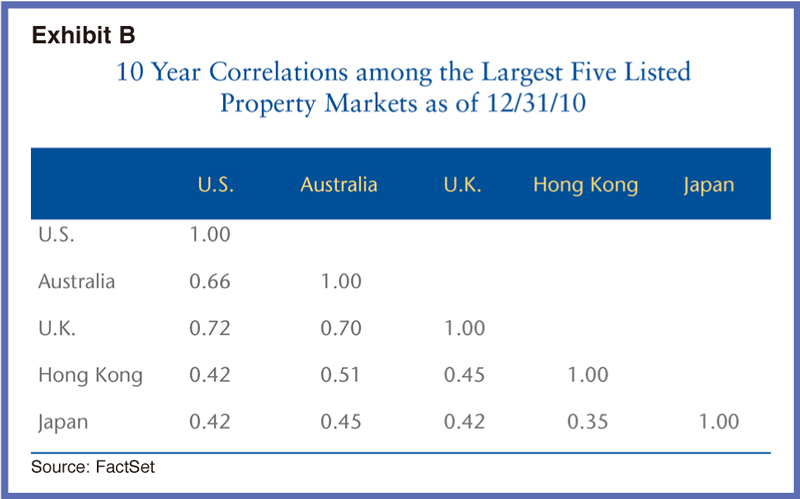

Global real estate securities also offer intra-asset class diversification. Real estate investing is a rather localised business because it is heavily influenced by market-specific factors (e.g. supply-demand profile, economic outlook, and interest rate environment). This means that real estate returns tend to differ from country to country over time. The differences in these returns lead to low correlations and, hence, potential diversification benefits. Exhibit B shows the 10-year correlations among the five largest listed property markets. With low correlations – in some cases, less than 0.50 – there is a tremendous opportunity to combine different markets to achieve higher risk-adjusted returns within the real estate allocation.

Inflation Protection

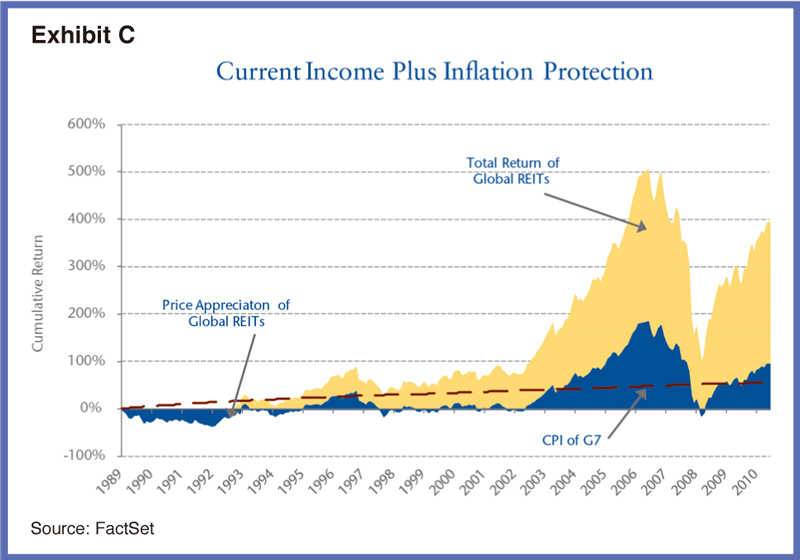

Over time, investment portfolios have to protect against the corrosive effects of inflation by allocating to assets that are either explicitly or implicitly tied to inflation. Real estate has historically served in that capacity because real assets like property tend to increase in value with the general level of prices. In listed property securities, inflation protection is a function of lease rollover (landlords earn higher rents and reimbursements, i.e. income streams, from tenants as leases rollover), and replacement cost support, i.e., the cost to construct buildings increases over time. Total returns in listed property securities come from two sources: price appreciation and current income/dividends. As seen in Exhibit C, over the past 20 years, the price appreciation of listed real estate has more than offset the general rise in costs, displaying the long-term inflation protection that real estate investing offers.

Yield and High Current Income

Global property securities also offer investors the benefit of current income, or yield – a trait that is particularly appealing in today’s low-yield world, where many investors are actively searching for attractive current income opportunities. While total returns for global listed real estate are a combination of current price appreciation and current income, Exhibit C also illustrates that, over the past 20 years, the vast majority of global real estate securities’ total return – over 75% – has come from dividends. Investors generally recognise dividends as a more stable driver of long-term performance.

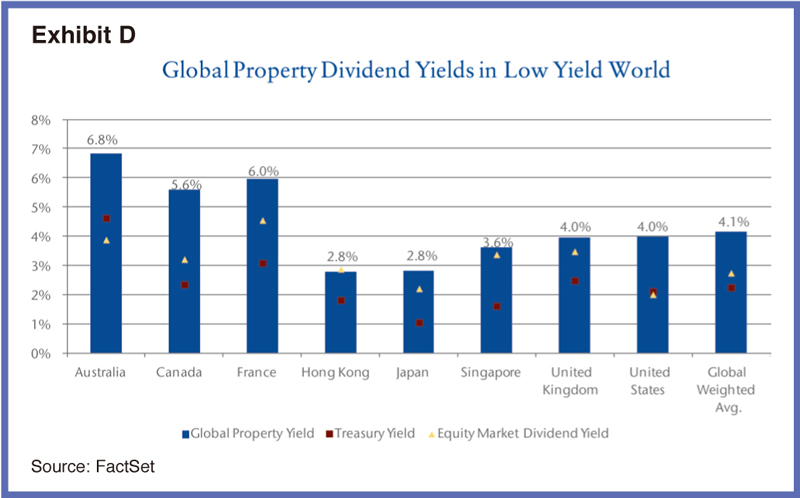

In Exhibit D, one can see that global property securities offer a sizeable advantage to both government bonds and general equities. We are also optimistic regarding dividend growth prospects for two reasons. First, while the global financial crisis put a dent in many property companies’ ability or willingness to pay dividends, we expect many of these companies to increase dividend payout ratios over the next few years, given greater credit-market stability. Second, as property markets continue to recover around the world, cash flows and earnings should rise, leading to dividend increases commensurate with this growth.

Conclusion:

With several long-term positive trends like world population growth, increasing urbanisation, and market share growth, there are demonstrable factors that support investment in global listed property. To investors, the benefits of allocating to this asset class are DIY: diversification, income, and yield.

Should you have any questions about global property securities, or how they can help enhance your portfolio, please contact your Principal Global Investors representative.

For more information, please contact

Principal Global Investors

Andrea Muller

Chief Executive, Asia

Tel: +65 64900 277

Email: [email protected]

Sameer Dev

Director, Head of Institutional Sales –

South & South East Asia

Tel: +65 64900 281

Mobile: +65 9680 9564

Email: [email protected]

Helen Chang CFA

Director, Head of Institutional Sales –

North Asia

Tel: +852 2596 7823

Mobile: +852 6898 0982

Email: [email protected]

Disclosures

The information in this document has been derived from sources believed to be accurate as of March 2011. It contains general information only on investment matters and should not be considered as a comprehensive statement on any matter and should not be relied upon as such. The information it contains does not take account of any investor’s investment objectives, particular needs or financial situation. Nor should it be relied upon in any way as forecast or guarantee of future events regarding a particular investment or the markets in general. All expressions of opinion and predictions in this document are subject to change without notice. Subject to any contrary provisions of applicable law, no company in the Principal Financial Group nor any of their employees or directors gives any warranty of reliability or accuracy nor accepts any responsibility arising in any other way (including by reason of negligence) for errors or omissions in this document.

This presentation is intended for sophisticated institutional investors only.